File

File

|

[Outlook on Global Affairs 2026-Special Issue No. 10] India in 2026: Sustained Growth amid Mounting Pressures and the Test of Strategic Autonomy |

| December 11, 2025 |

-

Yoon-Jung ChoiPrincipal Research Fellow, Sejong Institute | yjchoi@sejong.org

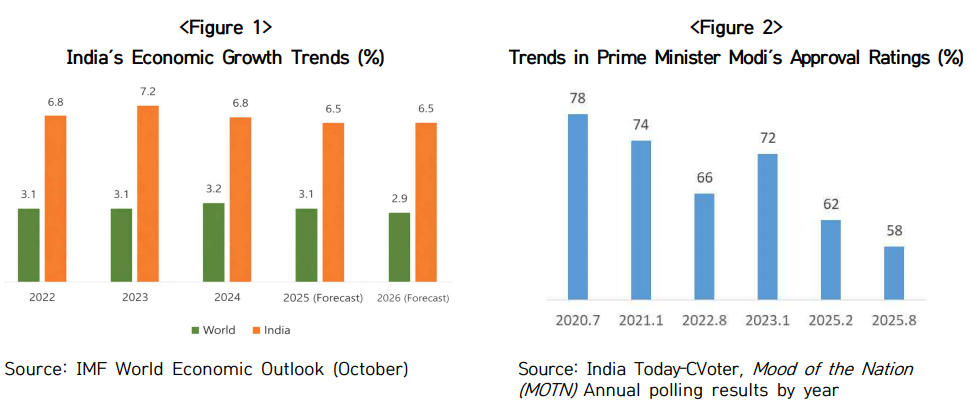

- In 2025, India consolidated its position as one of the world’s fastest-growing major economies, recording an estimated growth rate of approximately 6.5 percent, the highest among leading economies. Yet India confronted intensifying tests to both its high-growth momentum and strategic autonomy. The post-2024 coalition configuration, deepening socioeconomic fissures in rural and youth cohorts, and the transactional inflection in U.S. policy - manifest in Trump's tariff regime and the revised National Security Strategy (NSS) - collectively demanded a more deliberate recalibration of New Delhi's posture as it entered 2026.

-

Politics: Coalition Constraints and of Public Sentiment

Indian politics in 2025 was a process of seeking a new equilibrium built upon the structural legacy of the 2024 general election. Although the Bharatiya Janata Party (BJP) lost its single-party majority, it retained a majority within the National Democratic Alliance (NDA). Consequently, the third Modi administration became structurally beholden to coalition allies for the first time, creating a governing environment defined by continuous negotiation, consultation, and compromise across key policy domains, including cabinet formation, fiscal management, agricultural policy, welfare programs, and electricity pricing.1)

These dynamics were clearly illustrated in the Bihar state elections of November 2025. With Prime Minister Narendra Modi personally leading the campaign, the NDA secured a decisive 202 of 243 seats - a triumph that reaffirmed his enduring appeal in the Hindi heartland. At the same time, the outcome underscored a broader structural reality: the restoration of earlier patterns of single-party dominance appears increasingly difficult, reinforcing the persistence of coalition-era constraints.2)

A gradual decline in Prime Minister Modi’s approval ratings further contributed to political uncertainty. After consistently maintaining high levels of support, Modi experienced a marked decline in domestic polling throughout 2025, with his approval numbers slipping to the high-fifties by the second half of the year. This trend is narrowing the government’s political space for politically sensitive reforms or external concessions.

Socioeconomic grievances also emerged as a significant variable shaping political dynamics. Among university-educated youth in particular, persistent structural barriers to employment led to an expansion of short-term and non-regular jobs in major cities, while medium-sized cities and rural areas faced a continued shortage of job opportunities. These realities amplified dissatisfaction among young people and middle-class households, elevating employment frustrations into a salient political issue.3) These structural frustrations increasingly translated into a politically salient source of discontent, constraining the government’s room for maneuver not only in domestic reform but also in trade and external policy decisions.

Economy: Structural Vulnerabilities Amid Strong Growth

India recorded one of the fastest growth rates among major economies in 2025. Leading forecasters, including the International Monetary Fund (IMF), projected real GDP growth of approximately 6.5 to 6.6 percent.4) Despite a more challenging external environment, growth has been supported by a predominantly domestic-demand-driven economic structure, with private consumption accounting for an estimated 55 to 60 percent of GDP, augmented by infrastructure outlays, manufacturing incentives, digital public goods, and urban middle-class rebound. Labor market indicators point to mixed trends. As of October 2025, the labor force participation rate rose to the mid-55 percent range, its highest level in six months, and female employment continued a gradual upward trajectory.5) At the same time, the labor market remains characterized by a high share of self-employment and informal work, limiting improvements in job quality. Persistent constraints on the availability of stable employment for younger cohorts remain a potential source of social stress.

On income and consumption, indicators suggest a continued K-shaped recovery. Demand among higher-income households for passenger vehicles, air travel, online tourism, luxury retail, and premium education services has exceeded pre-pandemic trends. In contrast, consumption in lower-income and rural segments, including spending on essential goods, low-cost consumer products, and small-value prepaid mobile recharges, has remained flat in real terms or has recovered only modestly.6)

Concurrently observed trends include rural wage stagnation, increased demand for public employment programs under the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS)7) , declining savings among lower-income households, and rising asset prices in financial and real estate markets that disproportionately benefit higher-income groups. These dynamics appear to be contributing to widening socioeconomic disparities that may increasingly translate into political instability risks.

Structural constraints in the agricultural sector remained particularly salient. Agriculture continued to absorb roughly half of total employment while contributing approximately 16 percent of GDP, reflecting persistent underemployment and low productivity. In the aftermath of the pandemic, many workers who had returned to rural areas faced limited opportunities to re-enter nonfarm employment, heightening the political sensitivity of agricultural reform and reinforcing India’s cautious posture in trade negotiations involving agricultural market access.

Foreign Affairs and Trade: External Pressures and Strategic Recalibration

India’s foreign policy and trade environment in 2025 evolved within a complex landscape shaped by overlapping geopolitical and economic pressures. The most immediate source of strain stemmed from the Trump administration’s second-term tariff measures. Citing reciprocity, Washington imposed a baseline tariff of 25 percent on Indian-origin products and introduced an additional punitive tariff of 25 percent linked to India’s continued imports of Russian crude oil, bringing the combined tariff burden to 50 percent. These measures generated significant costs for Indian firms and policymakers, particularly given India’s exposure to the U.S. market. In addition, the National Security Strategy (NSS) released on December 4 identified India as a core Indo-Pacific partner, but framed cooperation less in terms of democratic solidarity or values-based alignment and more through a functional lens centered on commercial interests and security contributions.8) This orientation suggested that future bilateral negotiations would likely become increasingly transactional, reinforcing India’s incentives to recalibrate the relationship accordingly.

Against this backdrop, the U.S.-India “Phase One” bilateral trade agreement advanced toward its final negotiation stage. Discussions reportedly centered on tariff adjustments, agricultural access, energy cooperation, and digital regulatory frameworks. The United States sought expanded market access and greater rules-based commitments, while India pursued trade-offs involving surplus reduction and greater predictability in tax and tariff regimes.9)

India’s engagement with Russia also underwent calibrated adjustment. President Vladimir Putin’s December 2025 state visit reaffirmed bilateral cooperation in energy, defense, nuclear power, and critical minerals. India, however, adopted a carefully balanced posture, emphasizing long-term supply stability without explicitly reaffirming continued purchases of Russian crude.10) This posture reflects both structural constraints that may compel India to gradually reduce dependence on Russia over time and a political calculus aimed at signaling strategic autonomy, namely, that India does not align unconditionally with either Washington or Moscow. In the defense domain, the emphasis has increasingly shifted away from new large-scale procurement toward the stable operation and upgrading of existing projects, underscoring a clearer reality: even if Russia remains an important partner, it is unlikely to retain the near-exclusive position it once held in India’s defense portfolio.

India’s relationship with Pakistan also faced renewed strain following a terrorist incident in Kashmir in spring 2025, which reignited border tensions. India responded by tightening border management, expanding counterterrorism operations, and making Pakistani accountability a precondition for any resumption of dialogue.

In this context, Washington’s post-Pahalgam posture provoked domestic backlash in India, reflecting concerns over both its perceived mediative positioning and the appearance of Pakistan-leaning alignment. Such perceptions intersected with entrenched diplomatic red lines in Indian foreign policy, thereby reducing New Delhi’s concessions bandwidth and reinforcing structural skepticism toward the United States.11)

Relations with China featured a dual dynamic of limited easing alongside enduring structural competition. The two sides gradually restored senior-level dialogue that had been suspended following border clashes, and moved in stages toward selective confidence-building measures, including partial troop disengagement in certain border areas as well as the phased resumption of cross-border trade and direct flights.12) At the same time, China’s military buildup, expanded naval activity in the Indian Ocean, and growing influence across economic and technological domains have continued to generate persistent concern within India’s security community. India has sought to deter China and diversify supply chains through coordination mechanisms with the United States and its partners, including the Quad, IPEF, and I2U2, while simultaneously maintaining engagement through multilateral platforms such as BRICS and the Shanghai Cooperation Organisation (SCO).

Maritime security and the Indian Ocean posture also constituted a central pillar of India’s external strategy in 2025. Building on the SAGAR (Security and Growth for All in the Region) vision and the Indo-Pacific Oceans Initiative, New Delhi expanded cooperation with Indian Ocean littoral states on maritime domain awareness (MDA), disaster response, sea lines of communication (SLOC) protection, and infrastructure and connectivity initiatives. Joint exercises and intelligence-sharing arrangements with partners such as the United States, Japan, Australia, and France became increasingly routinized, enabling India to further consolidate its strategic presence across the Indian Ocean.

Taken together, India’s foreign affairs and trade environment in 2025 was shaped by the interaction of U.S. tariff pressure and trade negotiations, continued economic interdependence with China, and persistent tensions with Pakistan, while elevating the strategic salience of India’s Indian Ocean maritime agenda. At the same time, India appeared to adopt a more cautious posture, prioritizing national interests across most issue areas rather than positioning itself prominently as a mediator or global leader. Domestic political and economic risks, including coalition constraints, public sentiment, and uneven growth outcomes also appear to have narrowed India’s external policy bandwidth in increasingly visible ways. -

Politics and Society: Electoral Dynamics and Governance Pressures

India’s political landscape in 2026 is likely to be shaped by the dual imperatives of sustaining coalition stability and navigating the electoral dynamics of major state contests. While the Modi government demonstrated continued competitiveness within its core base through its victory in Bihar, it would be premature to interpret this outcome as evidence of a structural weakening of the opposition.

In states such as West Bengal, Tamil Nadu, and Kerala, anti-BJP and non-NDA forces retain strong organizational foundations. Several assessments suggest that opposition parties may continue to hold advantages across parts of southern India. State elections scheduled for 2026, including those in Assam, West Bengal, Tamil Nadu, and Kerala, will therefore serve as important political inflection points.

Should opposition forces consolidate their strength in key contests, the central government will face the simultaneous task of managing coalition partners while adapting differentiated electoral strategies to diverse state-level political environments. These domestic dynamics are also likely to reinforce structural constraints in foreign policy, requiring New Delhi to remain attentive to public sentiment and subnational political considerations when managing U.S. trade negotiations, China policy, and Pakistan-related strategy.

With Prime Minister Modi’s approval ratings exhibiting a a gradual downward trajectory, the persistence of structural socioeconomic challenges—including youth employment pressures, rural welfare demands, the expansion of precarious work, and uneven access to health and education services—is likely to heighten political sensitivity in 2026. In election-facing regions, the government may lean more heavily toward short-term, results-oriented measures such as targeted subsidies, welfare expansion, and accelerated infrastructure allocation.

While such measures may help stabilize political support in the near term, they could also generate pressures on fiscal sustainability and complicate longer-term growth strategies. Identity- and religion-related tensions will remain latent variables. However, the central political question for 2026 is likely to concern whether the government can sustain political legitimacy through a credible balance between economic performance and social inclusion.

Economic Outlook: Three Key Risks Amid Strong Growth

India is expected to maintain solid growth in the mid-to-high 6 percent range in 2026. While major forecasters cite U.S. high-tariff measures as a downside risk for external demand, they generally project India’s 2026 growth at around 6.2 to 6.5 percent, reflecting the country’s structurally resilient domestic demand base.13) Strong household consumption, sustained infrastructure investment, manufacturing promotion policies, the continued expansion of digital public infrastructure, and ongoing urbanization are likely to remain key drivers of growth. At the same time, India’s macroeconomic outlook will continue to face three interrelated risks: inflationary pressures, persistent inequality, and supply chain vulnerabilities.

First, inflation and energy-related cost pressures remain a central concern. Expectations surrounding U.S. and European interest-rate trajectories, geopolitical instability in the Middle East, reduced imports of Russian crude, and increased reliance on U.S.-origin LNG and LPG may raise India’s import bill and intensify pressure on the current account. Diversifying energy imports through trade negotiations with the United States may strengthen medium- to long-term supply security, but in the near term, contract pricing, shipping costs, and exchange-rate volatility are likely to add upward pressure on inflation.

Second, India’s K-shaped recovery is likely to persist. If asset gains and consumption among higher-income groups continue to accelerate while rural and lower-income households face stagnant incomes, the political sustainability of high growth could come under strain. If demand for MGNREGS remains elevated and employment gains are concentrated in informal or precarious jobs, the gap between headline growth performance and lived economic conditions could reemerge as a salient political issue in 2026.

Third, supply chain reconfiguration will continue to intersect with India’s structural dependence on China. Diversification strategies pursued by the United States, Europe, and Japan may generate new investment opportunities for India in sectors including semiconductors, electronics, batteries, and solar manufacturing. However, India’s continued reliance on Chinese intermediate inputs is likely to constrain the pace and scope of decoupling. India is therefore expected to pursue a calibrated adjustment strategy: expanding cooperation with partners in critical minerals, battery materials, and semiconductor equipment, while gradually reducing excessive dependence on Chinese components. Managing transitional cost increases and potential inflationary spillovers will remain a key policy challenge.

Foreign Policy and Trade: Strategic Rebalancing Pressures

In 2026, India’s foreign policy and trade agenda will likely be shaped by continued recalibration across its relations with the United States, Russia, and China. A central challenge will involve sustaining economic growth while preserving strategic autonomy, alongside consolidating India’s maritime position in the Indian Ocean.

First, in its relationship with the United States, a key priority will be the conclusion of the Phase I bilateral trade agreement that remained under negotiation through late 2025. As suggested in the 2025 U.S. National Security Strategy, Washington is expected to condition tariff relief not only on reductions in India’s imports of Russian crude, but also on expanded market access in sectors such as agriculture and digital services, as well as India’s alignment with U.S.-preferred standards on intellectual property and data governance. For India, this could yield more stable access to the U.S. market in sectors such as IT services, pharmaceuticals, auto parts, and certified “fair trade” goods, but it would also intensify domestic sensitivities over market opening in politically contested areas. In parallel, India is expected to accelerate diversification efforts to hedge against U.S.-driven volatility, including parallel negotiations or upgrades of trade arrangements with the European Union, ASEAN, and the Gulf Cooperation Council (GCC).

Second, India’s approach toward Russia is likely to remain anchored in continued energy cooperation, albeit with gradual adjustments in the composition of imports. While India has articulated ambitious targets - including expanding bilateral trade volumes and deepening cooperation in energy, nuclear power, and critical minerals - implementation will remain constrained by structural factors, notably growing exposure to U.S. tariff and sanctions risks, as well as Russia’s increasing dependence on China. A plausible trajectory for 2026 involves India gradually reducing the share of Russian crude within its import mix while retaining Russia as a strategic option, alongside expanded diversification toward the United States and Middle Eastern suppliers. Concurrently, India may continue to broaden its energy portfolio through increased imports of LNG and LPG, as well as greater emphasis on renewable energy.

Third, relations with China are expected to remain defined by a dual-track dynamic in which pragmatic engagement coexists with structural rivalry. New Delhi recognizes that abrupt exclusion of China from supply chains would complicate India’s near-term objectives in manufacturing expansion and green transition strategies. Simultaneously, concerns regarding China’s capacity for economic coercion continue to reinforce India’s emphasis on de-risking and diversification in strategically sensitive sectors. India’s China policy in 2026 is therefore likely to prioritize phased, sector-specific adjustments rather than comprehensive separation.

Fourth, India’s maritime strategy is expected to place sustained emphasis on cooperation with Indian Ocean littoral states, protection of sea lines of communication, maritime disaster response, and connectivity initiatives, including the development of “green ports.” These efforts will likely be supported by continued naval modernization, enhanced maritime domain awareness capabilities, and gradual expansion of force structure, including carrier and submarine assets. India is also expected to deepen joint exercises, intelligence-sharing mechanisms, and cooperation on countering illegal, unreported, and unregulated (IUU) fishing with partners such as the United States, Japan, Australia, and France. Collectively, these initiatives would function as a stabilizing and balancing mechanism within an increasingly contested Indian Ocean environment.

Finally, the prospect of a Quad leaders’ summit will be a key test of India’s diplomatic leverage in 2026. Although such a summit did not materialize in 2025 amid India–U.S. frictions, the possibility of India hosting it may reemerge. The year carries added significance as India is also scheduled to serve as the BRICS chair in 2026. Taken together, these overlapping diplomatic roles are likely to render 2026 a particularly consequential stage for India’s strategic balancing. If a Quad summit is held in India, major indicators to watch will include how New Delhi frames its positioning between structural competition and selective engagement with China and Russia, as well as how Quad initiatives on supply chains, maritime security, climate cooperation, and digital infrastructure are situated within India’s broader diplomatic narrative, particularly in relation to the Global South. -

In 2026, India is expected to remain one of the world’s most dynamic high-growth economies and an increasingly influential actor in multilateral diplomacy and Global South narratives. At the same time, structural constraints are likely to weigh more heavily on both domestic governance and external strategy, including coalition dynamics shaped by the 2024 general election, persistent vulnerabilities in youth employment and rural livelihoods, and the continued expansion of the informal sector. These overlapping pressures suggest that India is entering a phase requiring more cautious calibration in both domestic and external policymaking.

Externally, India’s policy environment will be defined by a complex interaction of challenges, including negotiations with the second Trump administration over elevated tariff regimes, burden-sharing pressures reflected in the U.S. National Security Strategy, sanctions and tariff exposure linked to energy cooperation with Russia, efforts to reduce structural dependence on China, persistent security tensions involving Pakistan, and the growing strategic salience of the Indian Ocean agenda. Taken together, these dynamics point toward India pursuing a form of cautious strategic autonomy as it advances its national interests.

South Korea’s own foreign policy is similarly entering a period that demands sustained strategic adjustment amid overlapping structural pressures. These include the deepening entrenchment of U.S.-China strategic competition, the persistence of the North Korean nuclear challenge, intensifying technological rivalry and supply chain restructuring, and the rising geopolitical and economic influence of the Global South. Seoul faces the dual task of managing alliance commitments while refining its strategic autonomy, strengthening economic and technological resilience, and reinforcing international norms and multilateral order as a middle power.

These structural conditions partially converge with the strategic challenges confronting India, thereby enhancing the underlying compatibility of bilateral cooperation. India is emerging as an increasingly important partner in domains closely aligned with South Korea’s core policy priorities, including economic security, supply chain resilience, and technological and industrial competitiveness. The structural drivers for deeper cooperation are therefore likely to strengthen further.

At the same time, India’s coalition politics, state-level dynamics, tensions arising from uneven growth outcomes, intensifying U.S. tariff and burden-sharing pressures, and exposure to Russia-related sanctions risks impose tangible constraints on both the pace and modality of bilateral engagement. The Lee Jae-myung administration’s effort to integrate interest-driven pragmatic diplomacy with the vision of a globally responsible state should be operationalized in a manner that fully leverages India’s growth potential, while maintaining a clear-eyed recognition of the underlying political, social, and external constraints shaping India’s strategic environment.

First, South Korea should position India as a strategic partner within a broader and more differentiated framework encompassing domestic consumption, digital public infrastructure, the green transition, and growth beyond major metropolitan centers. As the 2025 assessment indicates, India’s growth drivers increasingly extend beyond infrastructure expansion and urban middle-class demand, incorporating digital systems, welfare expansion, and rising demand for education and healthcare. Given the political significance of major state elections in 2026, South Korea’s engagement strategy should adopt a more multi-layered geographic and sectoral orientation, extending cooperation beyond established manufacturing and technology hubs to regions where infrastructure and social service demands remain substantial.

Second, South Korea’s cooperation framework should be designed with careful attention to how India’s domestic political and socioeconomic constraints shape external policy decisions. Core foreign economic policy issues - tariff negotiations with the United States, adjustments in energy partnerships, the pace of supply chain diversification from China, and Pakistan-related crisis management - are deeply intertwined with domestic variables such as agriculture, employment, inequality, and identity-based tensions. South Korean policymakers and businesses should therefore closely monitor how these internal constraints translate into regulatory adjustments, election-cycle policy risks, and sector-specific incentive shifts, while building greater flexibility into the structure of bilateral engagement.

Third, supply chain diversification and technology cooperation represent one of the most structurally complementary areas for bilateral engagement. India’s ambition to expand manufacturing capacity in strategic sectors—including semiconductors, batteries, electronics, electric vehicles, and renewable energy—aligns closely with South Korea’s comparative strengths in advanced manufacturing, components, and technological systems. Structured partnerships involving joint ventures, co-development initiatives, research collaboration, and critical minerals supply chains may generate mutually reinforcing gains in resilience, competitiveness, and market diversification.

Fourth, maritime security and defense cooperation represent one of the most promising domains for strategic alignment between South Korea and India. India, through SAGAR and related maritime initiatives, has prioritized the protection of sea lines of communication, maritime domain awareness, disaster response, and the strengthening of port infrastructure and connectivity. South Korea possesses comparative strengths in naval platforms, submarines, surveillance and reconnaissance systems, subsea infrastructure protection, and maritime cyber security for shipping and ports. In this regard, 2026 presents an opportunity to deepen cooperation through institutionalized security dialogues, working-level coordination, and targeted joint initiatives.

In sum, India’s trajectory in 2026 is likely to combine sustained high growth and expanding regional influence with structural constraints rooted in domestic political economy and an increasingly complex external environment. For South Korea, a strategy grounded in balanced expectations, realistic risk assessment, and forward-looking cooperation in supply chains, technology, and maritime security may enable bilateral relations to evolve into a durable pillar of South Korea’s broader Indo-Pacific and Global South strategy.

| India in 2025: An Assessment

| India in 2026: Key Strategic Watchpoints

| Implications for South Korea

1) John Reed, “Narendra Modi Defies Exit Polls to Secure Third Term,” Financial Times, June 4, 2024.

2) John Reed, “Narendra Modi Boosted by BJP Election Triumph in India’s Poorest State,” Financial Times, November 14, 2025.

3) Government of India, Ministry of Statistics and Programme Implementation, Periodic Labour Force Survey (PLFS), Monthly Bulletin, August 2025 (New Delhi: National Statistical Office, 2025), 12–18; Press Information Bureau, Government of India, "Periodic Labour Force Survey (PLFS) Monthly Bulletin August 2025," September 15, 2025.

4) International Monetary Fund, "World Economic Outlook," October 2025, 6.6%; World Bank, "South Asia Development Update," October 2025, 6.5%; Asian Development Bank, "Asian Development Outlook," July 2025, 6.5%.

5) Government of India, Ministry of Statistics and Programme Implementation, Periodic Labour Force Survey (PLFS), Monthly Bulletin, October 2025 (New Delhi: MOSPI, 2025).

6) Government of India, Ministry of Rural Development, “MGNREGA Public Data Portal,” accessed November 27, 2025, https://nrega.nic.in.

7) MGNREGS stands for the Mahatma Gandhi National Rural Employment Guarantee Scheme, a public employment program based on the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA), which the Government of India enacted in 2005.

8) The White House, National Security Strategy of the United States of America, November 2025 (Washington, DC: The White House, 2025), p. 20, “We must improve commercial relations with India to encourage New Delhi to contribute to Indo-Pacific security.”, https://www.whitehouse.gov/wp-content/uploads/2025/11/2025-National-Security-Strategy.pdf.

9) “First Phase of India–US Trade Deal Nearing Closure; to Address Tariff Issues: Official,” The Economic Times, November 17, 2025, https://economictimes.indiatimes.com/news/economy/foreign-trade/first-phase-of-india-us-trade-deal-nearing-closure-to-address-tariff-issues-official/articleshow/125385706.cms.

10) Ted Regencia and Joseph Stepansky, "Putin pledges 'uninterrupted' fuel shipment to India amid US sanctions," Al Jazeera, December 5, 2025, https://www.aljazeera.com/news/2025/12/5/putin-modi-kick-off-india-summit-as-trade-us-sanctions-loom-large.

11) 최윤정, "'트럼프 우선주의(Trump First)'와 인도의 인도-태평양 재조정," 『세종포커스』, 세종연구소, 2025년 9월 15일, https://www.sejong.org/web/boad/1/egoread.php?bd=1&itm=&txt=&pg=2&seq=12397.

12) International Institute for Strategic Studies, “Prospects for India–China Relations,” IISS Online Analysis, May 16, 2025, https://www.iiss.org/online-analysis/online-analysis/2025/05/prospects-for-indiachina-relations.

13) International Monetary Fund, "World Economic Outlook," October 2025, 6.2%; World Bank, "South Asia Development Update," October 2025, 6.3%; Asian Development Bank, "Asian Development Outlook," September 2025, 6.5%; OECD, "Economic Outlook," December 2025, 6.2%; Morgan Stanley, "India Economics and Strategy," May 2025, 6.5%.

※ The contents published on 'Sejong Focus' are personal opinions of the author and do not represent the official views of Sejong Institue